Effects from specified private pension

When deciding whether to pay into specified private pension, the key question is which of these options do you think is more important:

- Premium flexibility and inheritability with specified private pension

- A higher pension for the rest of your life and broader trauma insurance due to disability or death

Furthermore, keep in mind that the value of premiums in mutual insurance can be different depending on age and depending on whether it is paid in equal accruals or age-related. For fund members in equal accruals, for example, it is important to keep in mind that their accrual of rights in mutual insurance is higher than is generally the case and the value of premiums increases as the fund member is older.

For fund members in equal accrual who are 30 years or older, the specified personal pension will not result in higher total rights over the estimated retirement years. In age-related accrual, however, the rights accrual is more equal between mutual insurance and specified private pension.

You can see if you are in equal accrual or age-related accrual on My Pages.

See the effects with the Calculator

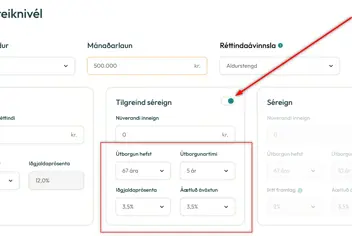

To see what effect it would have on your retirement rights to save in the specified private pension, it is best to use the Calculator on My Pages. Here is a step-by-step guide:

1.

Log in to My Pages and open the Calculator. All your information at LSR is pre-recorded in the Calculator.

2.

Enable the Specified Private Pension column. View the options and choose the one that suits you.

3.

In the "Estimated Results" window, you will see the estimated pension per month and both the monthly payout from the specified personal pension and the estimated total amount.

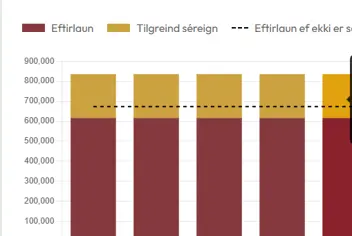

4.

In the histogram at the bottom of the page, you will see both columns for estimated pension per month and estimated payments from the specified private pension. There you will also see a dotted line that indicates the estimated pension for the rest of your life if you do not save into the specified private pension.

5.

By placing the mouse over the bars, you will see an information window that shows the numbers behind the histogram. The example below shows that by saving into the specified personal pension and paying it out during the first five years of retirement, this fund member will increase their payments during this five-year period from ISK 673,626 per month to ISK 835,575 (pension + specified personal pension). But after the specified private pension is used up, the payments will decrease to ISK 616,356 for the rest of their life.

Trauma insurance or flexibility?

In the end, the choice is always yours. The main advantage of specified private pension is primarily that the fund member creates inheritable assets and gets the opportunity to increase pension payments in the first years of retirement. But at the same time, it leads to lower pension payments in later years when payments of specified personal pension end, as well as reduced trauma insurance.

LSR therefore encourages fund members to familiarise themselves with the effect of choosing the specified private pension has on the lifelong pension and trauma insurance that can be obtained with full payments in mutual insurance. You need to keep both of these factors in mind in order to make an informed decision that suits you.